{kind=link}

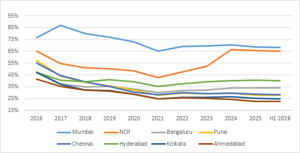

Mumbai, July 4th, 2026: Knight Frank India, in its proprietary report, Affordability Index, cited that homebuyer affordability remained broadly supportive across India’s residential markets during H1 2026, aided by the cumulative impact of 125 basis points of monetary easing. According to the Affordability Index, six of the eight tracked cities remain within the affordability threshold, while Mumbai Metropolitan Region (MMR) and the National Capital Region (NCR) continue to remain above the threshold of 50%. Ahmedabad once again emerged as the most affordable housing market among the top eight cities, with a ratio of 23%, followed by Kolkata at 25% and Pune at 28%.

Affordability worsened marginally in Bengaluru (35%) and NCR (65%) compared to 2025, while the remaining markets remained largely stable. Six of the eight tracked cities continue to sit within the 50% affordability threshold as a direct cumulative benefit of lower borrowing costs which is expected to continue supporting housing demand through H2 2026.

Knight Frank India’s Affordability Index, which measures the proportion of household income spent on EMIs, showed consistent improvement across the eight major Indian cities between 2016 and 2021. Affordability strengthened further during the pandemic as the Reserve Bank of India (RBI) lowered the policy repo rate to decadal lows. However, in response to elevated inflation, the RBI increased the repo rate by 250 basis points over a nine-month period beginning May 2022, which led to a deterioration in affordability during 2022.

Rate stability from early 2023 onward also helped stabilise affordability levels, but rising prices kept them elevated, particularly in the NCR. More recently, the RBI has delivered 125 basis points of cumulative easing ahead of the current pause, lending support to home loan affordability and helping residential sales sustain near the post-pandemic highs recorded in 2024. The Monetary Policy Committee (MPC) held the policy repo rate at 5.25% at both its February and June 2026 meetings, citing West Asia conflict-related energy price risks and uncertainty around monsoon conditions. With FY 2027 GDP growth revised to 6.6% and the CPI forecast raised to 5.1%, near-term rate stability appears the most likely scenario. The accumulated benefit of easing nevertheless continues to provide meaningful affordability support to homebuyers across most tracked markets.

Shishir Baijal, International Partner, Chairman and Managing Director, Knight Frank India said, “Housing affordability remains a key driver of residential demand. The cumulative benefit of lower interest rates continues to support homebuyers across most markets, helping sales remain close to post-pandemic highs. Over the year, affordability gains have moderated mostly due to the rise in property prices. However, healthy employment, stable incomes and supportive financing conditions continue to underpin demand. Going forward, sustained income growth and balanced market fundamentals will be critical to maintaining housing affordability and supporting long-term market growth.”

Affordability Index of Leading Eight Cities of India

| City | EMI to Income Ratio | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 2016 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | H1 2026 | |

| Mumbai | 77% | 77% | 73% | 65% | 69% | 70% | 71% | 69% | 69% |

| NCR | 65% | 50% | 49% | 43% | 48% | 52% | 66% | 66% | 67% |

| Bengaluru | 48% | 35% | 33% | 30% | 32% | 32% | 34% | 34% | 35% |

| Pune | 57% | 36% | 32% | 28% | 30% | 29% | 30% | 28% | 28% |

| Chennai | 55% | 35% | 31% | 28% | 30% | 29% | 30% | 29% | 29% |

| Hyderabad | 47% | 41% | 39% | 36% | 37% | 39% | 40% | 41% | 41% |

| Kolkata | 47% | 32% | 29% | 25% | 26% | 26% | 26% | 25% | 25% |

| Ahmedabad | 42% | 31% | 29% | 25% | 26% | 25% | 24% | 23% | 23% |

Source: Knight Frank Research. Note: For H1 2026, affordability levels are calculated keeping all variables constant, except for the interest rate and property price.

Note: The Knight Frank Affordability Index indicates the proportion of income that a household requires, to fund the monthly instalment (EMI) of a housing unit in a particular city. An EMI/Income ratio over 50% is considered unaffordable as it is the limit beyond which banks rarely underwrite a mortgage.

Note: The series reflects updated affordability index level, which accounts for revised methodology on residential prices.

Assumptions:

EMI, housing unit size and price/sq ft represent city-level averages.

Loan Tenure – 20 years

Loan to Value – 80%

Home loan interest rate – Average home loan rates

Area of housing unit: House size is fixed for each city across the years but varies within different cities taking into account the average size preference for each city.

Housing Price: Weighted average price based on unsold inventory for that city.

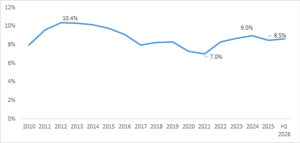

EMI to Household Income Chart

Source: Knight Frank Research

India’s residential market continues to benefit from stable employment, urbanisation and supportive financing conditions. These structural drivers remain intact despite heightened global uncertainty.

While geopolitical developments and inflationary pressures may influence sentiment in the near term, the cumulative benefit of monetary easing and healthy domestic fundamentals are expected to continue supporting housing demand across most major cities.

Housing Loan Interest Rate Chart

Source: Knight Frank Research

About Knight Frank

Knight Frank LLP is a leading independent, global property consultancy. Headquartered in London, Knight Frank has 20,000+ people operating from over 600+ offices across more than 50 territories. The Group advises clients ranging from individual owners and buyers to major developers, investors, and corporate tenants. For further information about the Company, please visit www.knightfrank.com

Knight Frank India is headquartered in Mumbai and has more than 2,000 experts across Bangalore, Delhi, Pune, Hyderabad, Chennai, Kolkata, Ahmedabad, Indore and Kochi. Backed by strong research and analytics, our experts offer a comprehensive range of real estate services across advisory, valuation and consulting, transactions (residential, commercial, retail, hospitality, land, and capitals), facilities management and project management. For more information, visit www.knightfrank.co.in